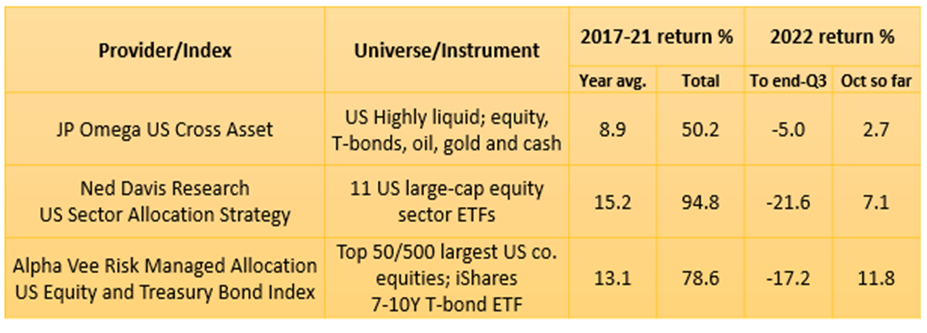

‘Long Only’ on the C8 Platform

The C8 platform has a broad range of ‘long only’ strategies, both developed in-house and from external providers. In the table below, we highlight the October bounce-back for some of the external provider indices in the context of Q1-Q3 losses and 2017-21 gains (more detailed analytics can be found on the C8 website). In the latest month, both JP Omega and Alpha Vee strategies have been able to recover over the half of the losses sustained over Q1-Q3 . In the case of JP Omega these losses were rather modest in any case – reflecting an allocation process that aims to pre-emptively manage risk levels. The Ned Davis US Sector Allocation Strategy invests purely in large-cap equity sector ETFs and has thus seen a more volatile year than cross-asset strategies. The Strategy outperformed the overall S&P 500 index over the first three quarters of Q3 (-21.6% vs -24.8% for the index) and broadly matched the October index bounce.