|

C8 Weekly Bulletin: Giving Investors an Edge11 October 2022 |

|

The US Q3 earnings season is now in full swing with Pepsi due to report midweek and a raft of major banks on Friday. This Bulletin takes a look at corporate debt market dynamics heading into the earnings season – with our index provider ExtractAlpha set to give their ‘big data’ earnings insights next week. |

|

|

US Earnings and the Corporate Balance Sheet |

|

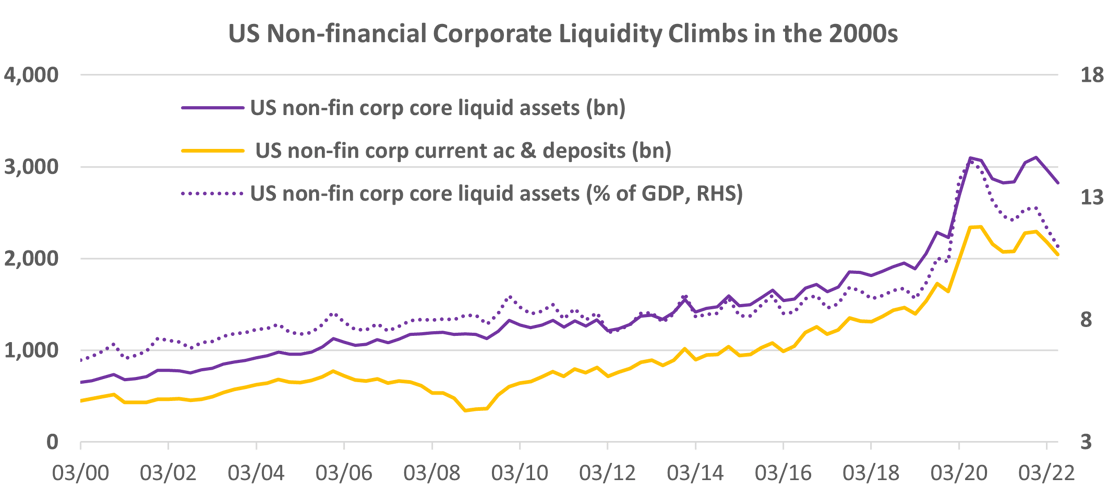

Upcoming corporate earnings reports will be watched closely not just for signs of the economic slowdown on quarterly sales but also the impact of a less favourable economic/ market backdrop on corporate balance sheets. Liquid assets of non-financial corporates peaked at $3.1trn at end-2021 and the steady retreat so far this year may be extended into Q3. Overall liquidity levels still look comfortable by the standards of the 2000s and while corporate debt levels have also climbed, net corporate debt levels are not stretched. Given high cash balances and profitability (Q2 was a sector record), US corporates may be well-placed to ride out any near-term mild outright recession. |

|

|

The near-term trajectory for corporate balance sheets is in particular focus as market repricing has substantially boosted returns from short-maturity credit exposure. The iBoxx $ Non-Financials BBB yield for the 1-3yr sector, for example, has climbed from 1.5% at start-year to 5.6%, and the pick-up from extending exposure beyond this (into 7-10yr) has been halved. While CTA/ trend strategies perform particularly well amidst major economic/ geopolitical shocks, short tenor corporate bond holdings may now provide steady – arguably attractive – returns if we see more stable outcomes for the US economy. |

|

|

|

Rates Products on C8 Studio |

|

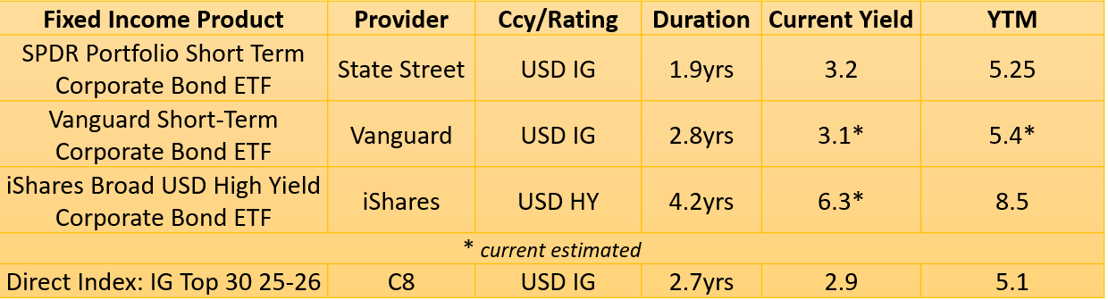

The rates products on the C8 platform are very diverse, ranging from cross-asset allocation to direct bond investment portfolios based on the S&P iBoxx bond indices. Selected ETFs with shorter fixed rate corporate exposure are shown in the table below (note that issuers in USD may be from outside the US). Directly invested bond portfolios may also have some advantages in this context as they allow a more precise positioning for specific credit and duration risks. As an illustrative example, a small bond portfolio of just the 2025/26 issues in the iBoxx USD Liquid IG Top 30 index trades on a 5.1% yield. |

|