Portfolios with both bonds and equities are traditionally called balanced portfolios, as these two asset classes often move in opposite directions, producing a more stable overall performance. This changed post the 2007/08 Global Financial Crisis when central banks around the world drove bond yields to unprecedented lows (by buying their own debt) to encourage capital back into riskier assets. This was an explicit goal of QE, to quote the Bank of England’s website:

“Here’s an example. Say we buy £1 million of government bonds from a pension fund. In place of those bonds, the pension fund now has £1 million in cash. Rather than hold on to that cash, it will normally invest it in other financial assets, such as shares, that give it a higher return. In turn, that tends to push up on the value of shares, making households and businesses holding those shares wealthier. That makes them likely to spend more, boosting economic activity.”

https://www.bankofengland.co.uk/monetary-policy/quantitative-easing

With the EUR crisis, and more recently, the Covid shock, the opportunity was lost to unwind this intentional boost to asset prices before inflation took hold. As central banks now rush to tighten policy, the inverse of the above policy is deflating both bond and equity prices.

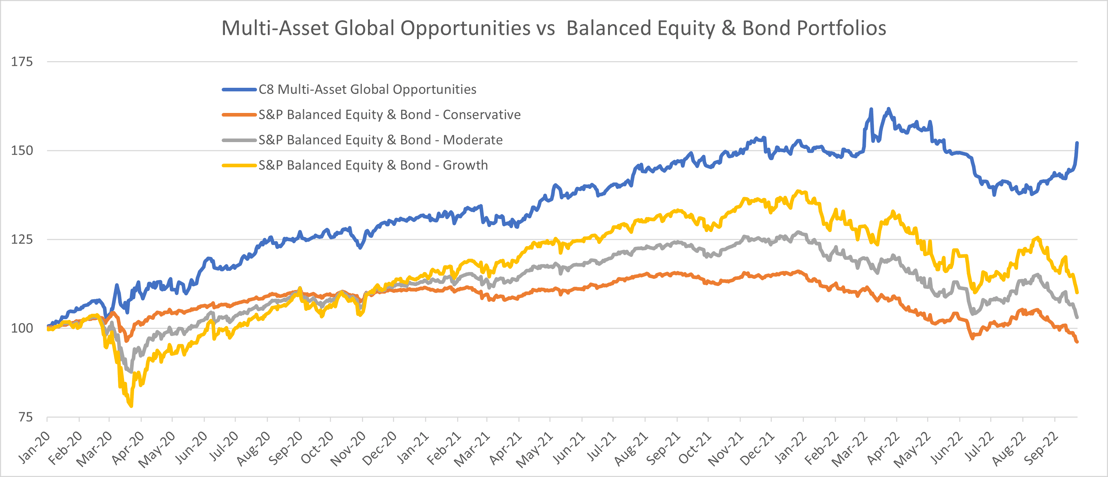

Historically, alternative indices can perform well in this environment, and, in the chart below, we compare how a multi-asset alternative strategy has compared to these balanced portfolios over the past three years. Whilst September was a difficult month for both stocks and bonds, the C8 Multi-Asset Global Opportunities certificate rose 3.9% (this contains alternative strategies from a number of providers on C8 Studio). Interestingly given recent events, the conservative portfolio (75% bonds, 25% equity) has been the worst performer. This illustrates that there was nothing ‘conservative’ about bonds when yields were at artificially low levels.