Market Recap

The “On-Again, Off Again” tariff game played heavily into yesterday’s market action. This is to say that, as we already know, freer markets are happy markets. Small caps led the way, with the Russell 2000 rising 2.55%. Exposure to Mag 7 and technology in general was additive, evidenced by the Dow gaining 1.42%, the S&P 500 adding 1.76%, and the Nasdaq Composite closing 2.27% higher. Indeed, 6 of the Mag 7 names (excepting Microsoft [MSFT]) featured in the top 10 contributors to the performance of the SPDR S&P 500 ETF Trust (SPY) with the remaining slots filled in by Eli Lilly (LLY), JP Morgan Chase (JPM) and Visa (V).

All sectors except Utilities (-0.18%) were higher, and Consumer Staples were essentially flat as staples producers like Kimberly Clark (KMB), Kraft Heinz (KHC), and Proctor & Gamble (PG) posted losses that were just about offset by gains from staple retailers like Costco Wholesale Corp (COST), Walmart (WMT), and Target (TGT). Consumer Discretionary saw the largest jump, rising 2.98%, buoyed by Amazon (AMZN) and Tesla (TSLA) combining to contribute to 66% of the sector’s result.

The Cboe Market Volatility Index (VIX) continued to retreat, falling just over 9% to close at 17.48 but despite this, gold remained elevated, trading at $3,008.80/oz in the early evening. Oil traded higher in the overnight session as news broke that Iranian oil tankers have been using forged Iraqi paperwork to evade sanctions.

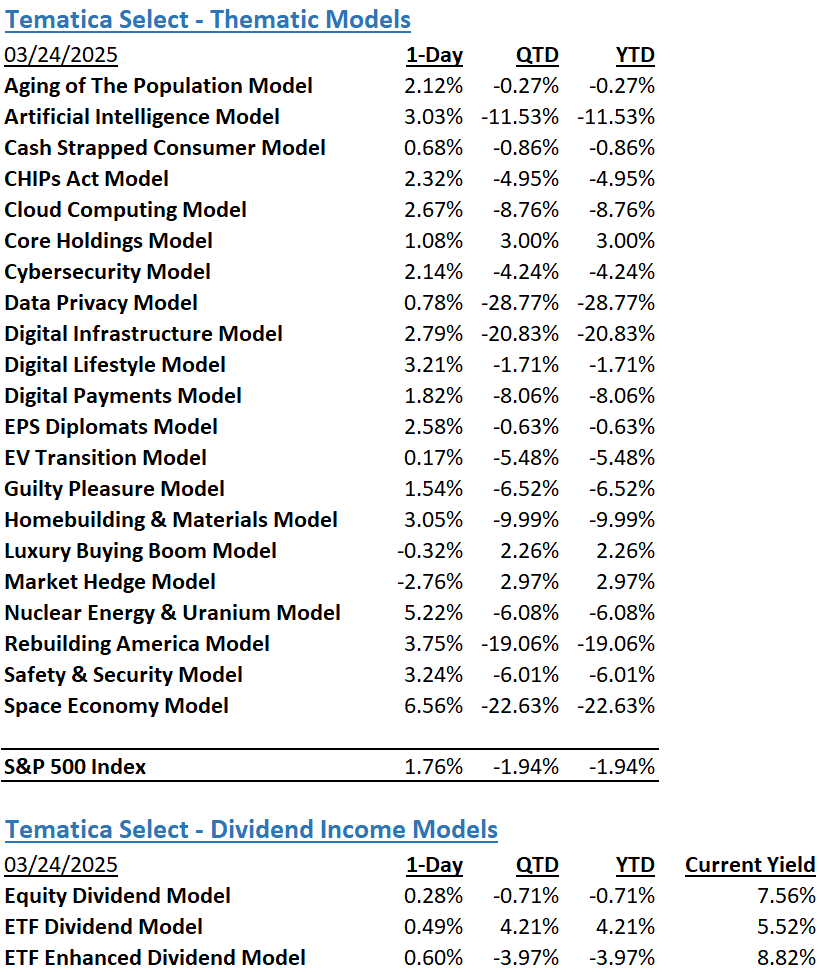

The Tematica Select Model Suite saw positive results across the board with the expected exclusion of Market Hedge which gave back about half of its 8% quarter-to-date excess return over the S&P 500 Index as of Friday’s close given the broad index’s rally. Leadership in the suite came from Space Economy and Nuclear Energy & Uranium.

Trump and April Tariffs – Will He or Won’t He?

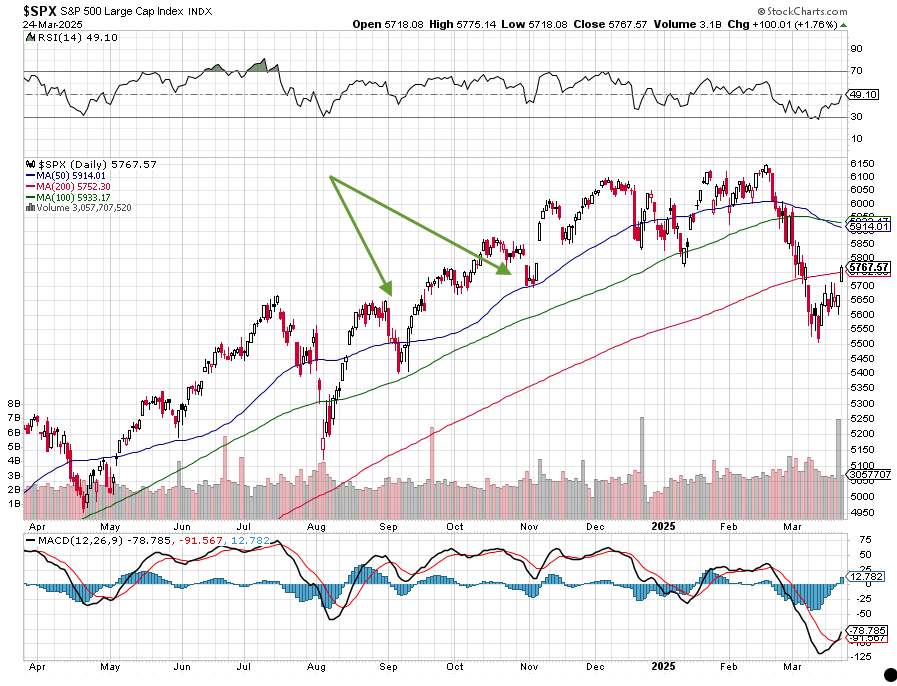

Following yesterday’s pop in the market, futures point to equities giving a fraction of those outsized gains back this morning. That move, which was fueled by potentially less-than-feared April Trump tariffs, led the S&P 500 to move even further away from being oversold and closing over its 200-day moving average. The question is does that become a level of support for the S&P 500? If the answer is “yes” that market barometer has the potential to climb another 3% or so until it hits another wall of resistance between 5,914-5,933. That would be enough to land the S&P 500 in positive territory on a year-to-date basis.

Ahead of Trump’s April 2 line in the sand, European Union trade chief Maros Sefcovic is scheduled to meet Tuesday with Commerce Secretary Howard Lutnick and US Trade Representative Jamieson Greer. Also, ahead of the day, Trump is calling “Liberation Day”, India’s government is likely to see tariff exemptions as part of scheduled bilateral trade talks early next week.

Would it be like Trump to announce trade deal wins and a smaller set of tariffs, touting it as a win? Let’s remember, the president fancies himself a great deal maker, so it is possible. And while Trump has downplayed the stock market’s February slide and the potential impact of tariffs on the economy, he has historically used both as a barometer of his presidential performance. Should that be the outcome we get, we could see the market’s relief rally continue.

However, if that isn’t the outcome, the impact of tariffs that are put in place and countries on the receiving end to respond in kind, odds are high companies will serve up disappointing June quarter guidance in the coming weeks. The ensuing pressure on 2025 EPS expectations for the S&P 500 would rekindle valuation questions, and likely lead to a bumpy patch in the market similar to what was experienced with the S&P 500 in September and October of last year.

This means over the next several days, investors will be focused on Trump’s comments even as we get the next pieces of economic data, and potentially at least some negative earnings pre-announcements. Since we’ve laid out some potential scenarios for the coming days, as evidenced in The Art of the Deal the president believes that being bold, assertive, and sometimes unpredictable keeps opponents off balance, giving him an upper hand. While Trump may be comfortable in that landscape, it’s far less comfortable to Wall Street, which prefers predictability.

The Strategies Behind Our Thematic Models

- Aging of the Population – Capturing the demographic wave of the aging population and the changing demands it brings with it.

- Artificial Intelligence – Software, chips, and related companies that facilitate the collection and analysis of large data sets and autonomous generation of solutions given non-machine language prompts.

- Cash Strapped Consumers – Companies poised to benefit as consumers stretch the disposable spending dollars they do have.

- CHIPs Act – Capturing the reshoring of the US semiconductor industry and the $52.7 billion poised to be spent on semiconductor manufacturing.

- Cloud Computing – Companies that provide hardware and services that enhance the cloud computing experience for users, such as co-location, security, and edge computing.

- Core Holdings – Companies that reflect economic activity and are large enough to not get pushed around by day-to-day market trends. Low-beta, large-cap names able to better withstand economic turmoil.

- Cybersecurity – Companies that focus on protecting against the penetration of digital networks and the theft, ransom, corruption, or destruction of data.

- Digital Infrastructure & Connectivity – Companies that are integral to the development and the buildout of the infrastructure that supports our increasingly connected world.

- Digital Lifestyle – The companies behind our increasingly connected lives.

- Data Privacy & Digital Identity – Companies providing the tools and services that verify authorized users and safeguard personal data privacy.

- EPS Diplomats – Profitable large capitalization companies proven to produce above-average EPS growth and provide investors with the benefit of multiple expansion.

- EV Transition – Capturing the transition to EVs and related infrastructure from combustion engine vehicles.

- Guilty Pleasure – Companies that produce/provide food and drink products that consumers tend to enjoy regardless of the economic environment and potential long-term health hazards associated with excessive consumption.

- Homebuilding & Materials – Ranging from homebuilders to key building product companies that serve the housing market, this model looks to capture the rising demand for housing, one that should benefit as the Fed returns monetary policy to more normalized levels.

- Market Hedge Model – This basket of daily reset swap-based broad market inverse ETFs protects in the face of market pullbacks, overbought market technicals, and other drivers of market volatility.

- Nuclear Energy & Uranium – Companies that either build and maintain nuclear power plants or are involved in the production of uranium.

- Luxury Buying Boom – Tapping into aspirational buying and affluent buyers amid rising global wealth.

- Rebuilding America – Turning the focused spending on rebuilding US infrastructure into revenue and profits.

- Safety & Security – Targeted exposure to companies that provide goods and services primarily to the Defense and security sectors of the economy.

- Space Economy – Companies that focus on the launch and operation of satellite networks.

The Strategies Behind Our Dividend Income Models

- Monthly Dividend Model – Pretty much what the name indicates – this model invests in companies that pay monthly dividends to shareholders.

- ETF Dividend Model – High-yielding ETFs that provide a range of exposures from domestic equities, international equities, emerging market equities, MLPS, and REITs.

- ETF Enhanced Dividend Model – A group of high-yielding ETFs that utilize options to enhance yield through collecting option income.

Don’t be a stranger

Thanks for reading and if you have a suggestion for an article or book we should read, or a stream we should catch, email us at info@tematicaresearch.com. The same email works if you want to know more about our thematic and targeted exposure models listed above.