C8 Monthly Update – January 2020 |

|

|

Skandinaviska Enskilda Banken AB (SEB) joins the C8 PlatformWe are delighted to announce that SEB have partnered with C8, so that their widely-respected Quant Indices will now be available on the C8 platform. SEB is the leading Nordic investment bank, with a large and successful Quant group, that provides both Indices and customised solutions across the Nordic region. SEB place great emphasis on sustainability, indeed they have been assessed as one of the world’s 100 most sustainable companies. This aligns well with a key benefit of using the C8 platform, having full transparency of the underlying assets in a portfolio ensuring asset owners can promote sustainability in the investment decisions. Our collaboration with SEB adds further momentum to C8’s Nordic sales effort run from Stockholm by Stefan Moberg, who was previously a senior sales manager at both Catella and Nordea Investment Management. |

|

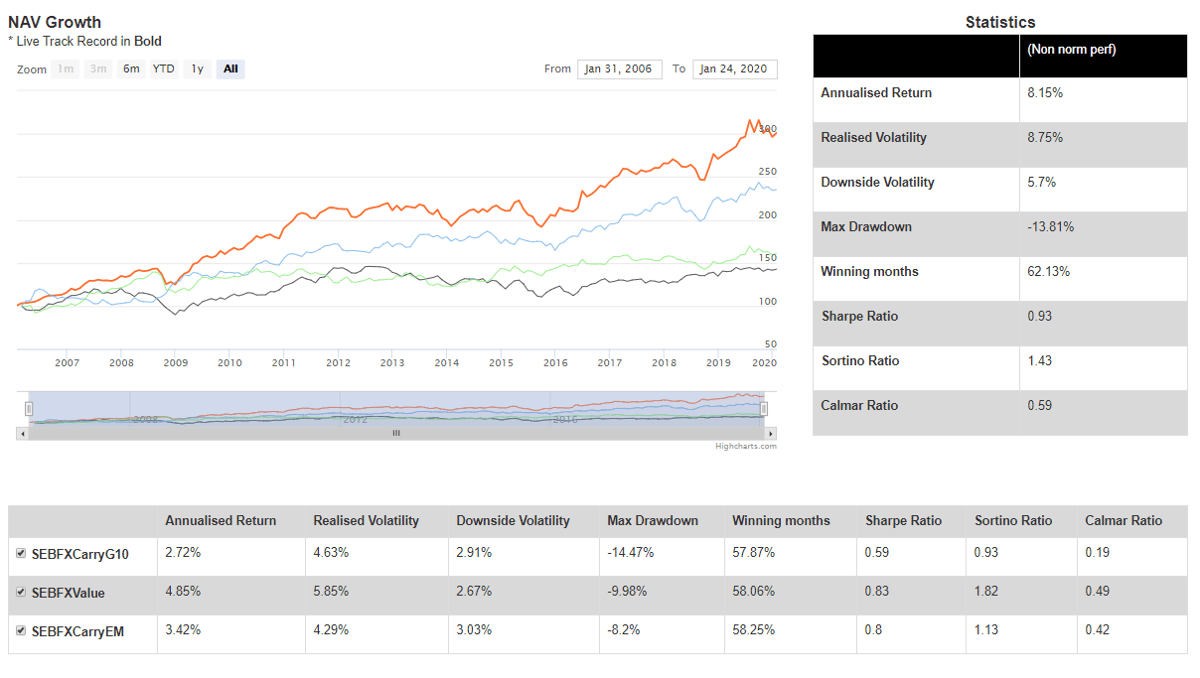

We are initially adding SEB’s FX and Equity Indices. In particular, we note that SEB FX Indices have been trading out of sample since 2014, and combining their Value and Carry Indices together would have produced a strong monthly performance (see chart below). |

|

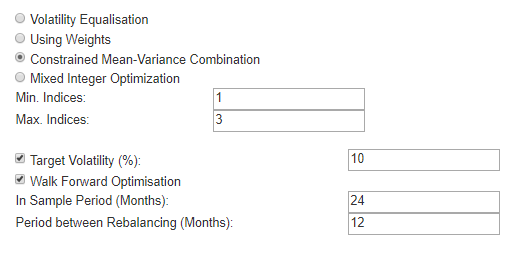

Combining SEB FX Indices with Other Providers, with Walk-Forward AnalysisHowever, we have also previously discussed that one of the key advantages of the C8 platform is the power of combining Indices from different providers (see the July 2019 Update), with capital only needed for the net portfolio positions (rather than for each Index using sub-allocation). We are pleased to announce that we have upgraded our combination functions to utilise ‘walk-forward’ analysis. We believe this produces a more robust combination as the performance is generated out of sample, reducing the risk that portfolios are simply optimized to best reflect past performance. The screenshot below shows the added functionality in ‘Combine Indices’ at the bottom of the ‘Available Indices’ page. In this case, the combination is made using classic Markovitz Mean-Variance optimization. The target volatility of 10% is chosen and, for the walk-forward, the sample period of the previous 24 months is chosen, with the process repeated every 12 months. In addition, each of the the Indices in the mean-variance calculation can be given a minimum and/or maximum weight to produce a more balanced portfolio. |

|

|

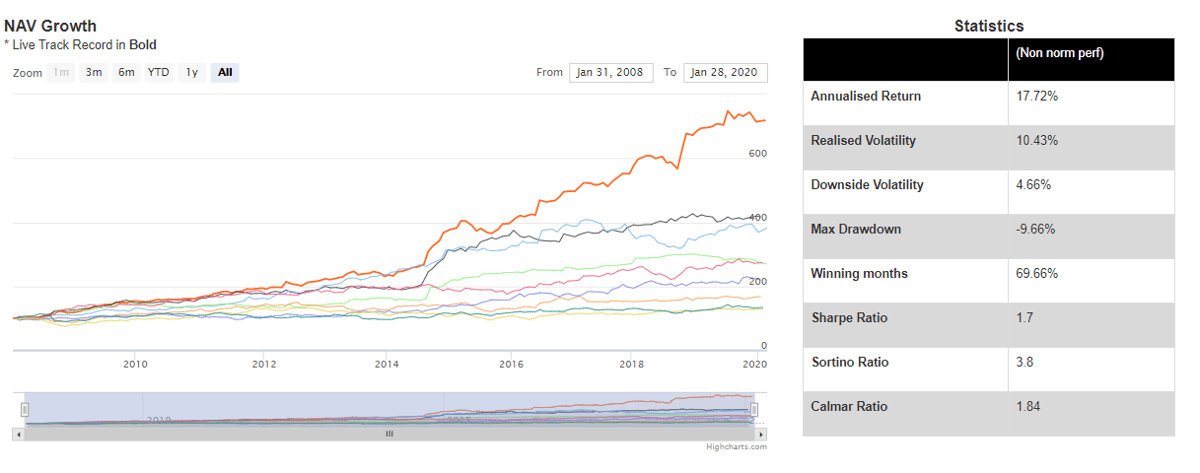

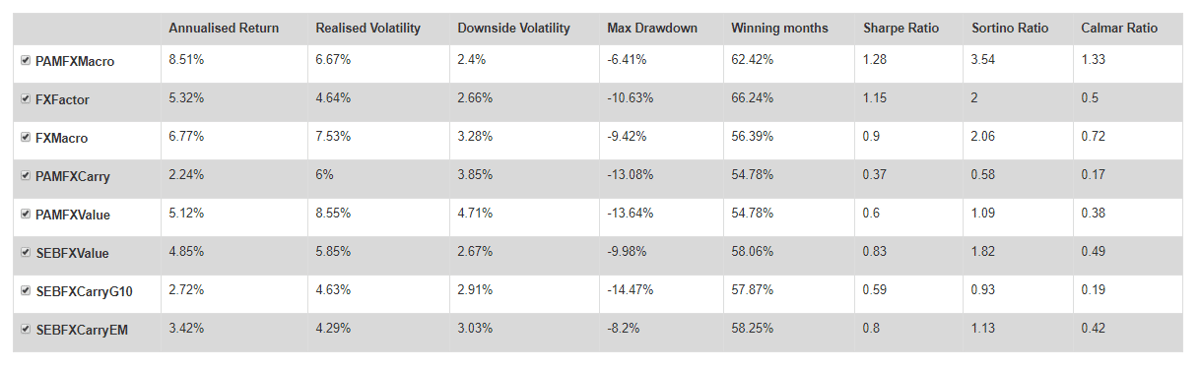

Indeed, with largely uncorrelated returns in the eight FX Indices, a number of clients are starting to use a combination of SEB, C8 and Pacific Asset Management FX Indices. The historic returns of a potential combination, combined using mean-variance with the ‘walk-forward’ functionality, is shown below: |

|

|

|

Also of note is that, in this case, the walk-forward realised vol of 10.4% (above) is close to the targeted volatility of 10%. |

|

|

|

|

C8 Studio – The Knowledge Hub |

|

The second upgrade to C8 Studio this month is the addition of a ‘Knowledge Hub’. This means that clients can now access monthly reports and updates from our Index Providers. The C8 Monthly Update can also be found here. This should prove to be a valuable resource to track the methodology and performance of Indices over time, as well as providing a reference for background information on the Index Providers. Index Providers update the Hub directly, and the Knowledge Hub is easily accessible from the C8 Studio menu. |

|

|

|

|

|

C8/GreenBlue Good Governance US Equity L/S Certificate Now Trading on the Frankfurt Stock ExchangeCirdan Capital have launched a certificate based on the C8/GreenBlue ESG Index. The Index is, of course, available to trade directly on the C8 platform, but is now also available for private clients of Wealth Managers etc on the Frankfurt Exchange. Please see the link below to track performance: |

|

|

|

C8 will be attending the Assiom Forex on 7-8 FebruaryPlease catch up with C8 at the Assiom Forex conference in Brescia next week. You will find us by the Morningstar stand, we would be delighted to meet you there. |

|

Thanks for reading, The C8 Team |

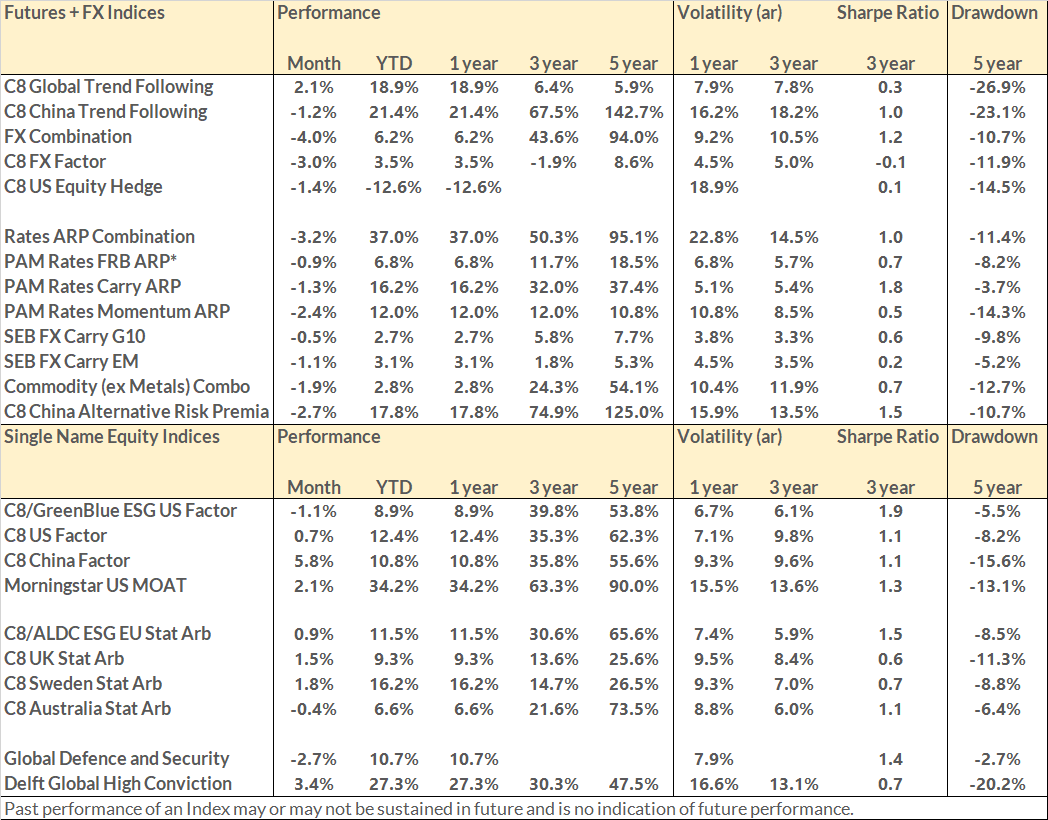

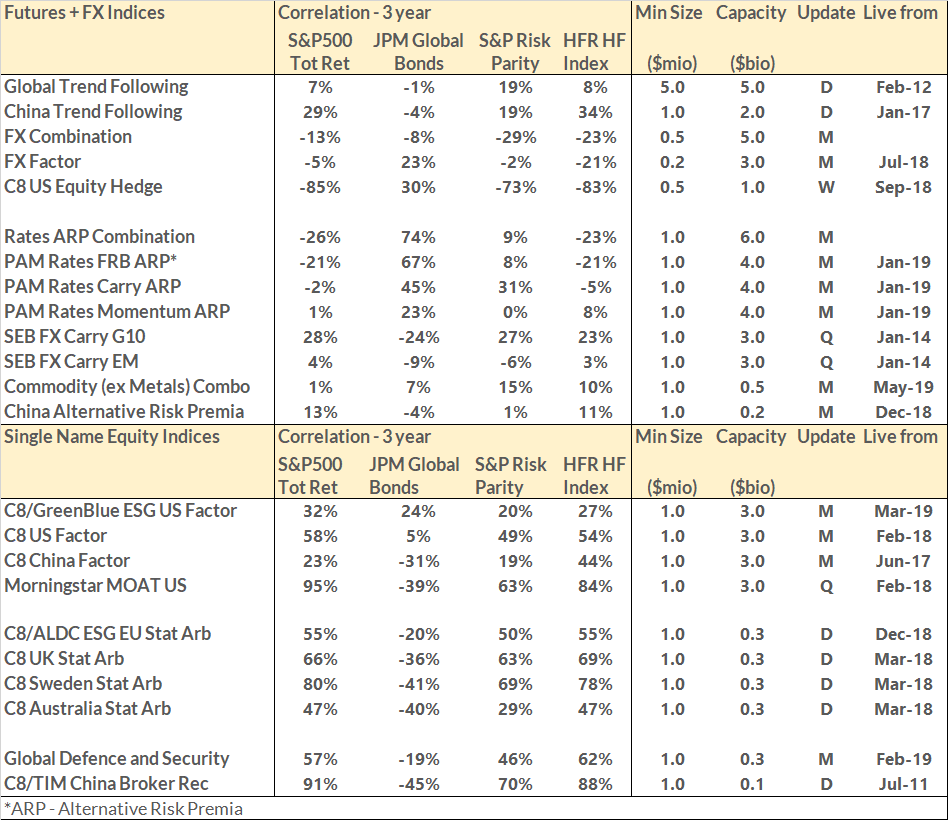

December 2019 PerformanceThe end of the 2019 gives us a chance to review the performance of the Indices on the C8 platform over the past year. Overall, it was a strong year for trend-following, interest rates risk premia and our equity indices. FX risk premia and commodities also produced positive returns, whilst China was a standout performer in trend-following and risk premia Indices in their commodity markets. January has suggested that 2020 may be a more complicated year, however risk premia has started the year well, suggesting that alternative investments may have value in these more difficult markets. |

|

|

|

|

|

|

| C8 Technologies, Michelin House, 81 Fulham Road, London, SW3 6RD, UK, +44 (0) 20 3826 0045 |

|