Power of Combination II: Tactical Asset Allocation

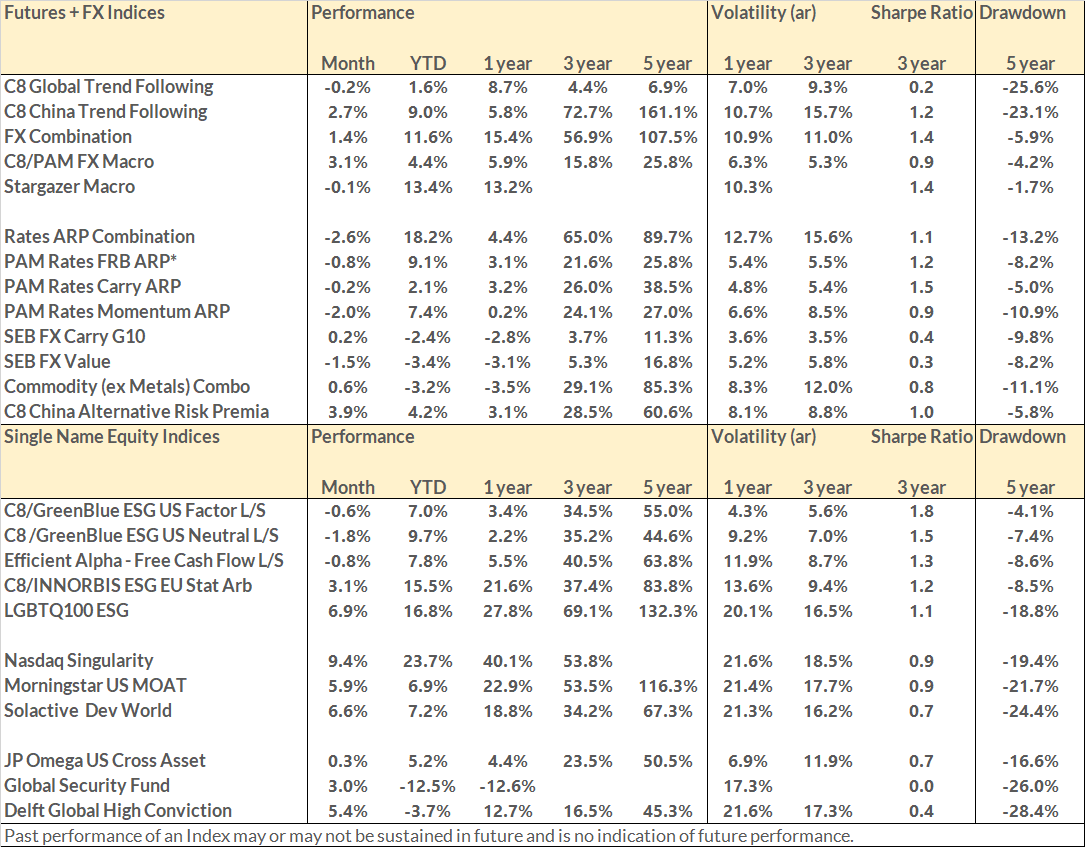

In May, we highlighted one of the major strengths of C8 Studio by focusing on the ‘power of combination’ in C8 Studio. In particular, we used Risk Parity to produce Alternative Risk Premia (ARP) combinations across 3, and then 5, asset classes.

We have now released a new combination algorithm, Tactical Asset Allocation (TAA). In this case, instead of using a Risk Parity weighting across our 5 ARP combinations, we determine what combination of indices would produce the most consistent performance. In contrast to risk parity, which gives an equal risk-adjusted weight to each component of the portfolio, or mean variance, which always looks for the highest risk return, TAA focuses consistency.

Indeed, unlike classic Mean-Variance, which overweights an outperforming index, Tactical Asset Allocation will underweight both an underperforming and outperforming index. We feel this has advantages over the more traditional approaches, given that, after a period of outperformance, there is a high probability of reversion to the mean. Therefore, both outperforming and underperforming strategies have their weight reduced.

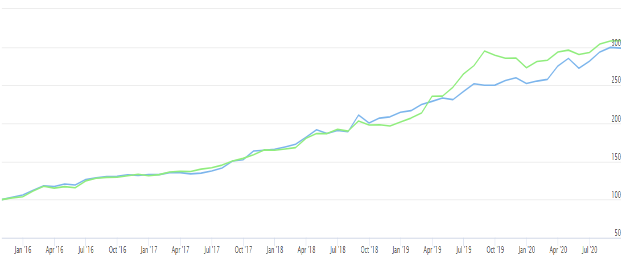

The chart below shows how the TAA performance (blue line) compares to the Risk Parity solution (green line). The index is rebalanced each year, looking back over the previous 2 years, using the same five ARP combinations that were the focus of the May 20 ‘Monthly Update’:

- Rates Combination

- FX Combination

- Commodity Combination

- US Good Governance Equity

- China Commodities (Accessed from Offshore)