Our friends at IVI Capital have produced some important research on how US debt limit dynamics can impact US (and Global) markets this year. In particular, the rundown of US Treasury cash holdings, since reaching the statutory debt limit on 19 January, is currently pushing liquidity into the US financial system. However, attention will soon turn to the impending cliff-edge in June (as ‘extraordinary measures’ are exhausted). Even after resolution, this will lead to a sharp tightening in US monetary conditions as Quantitative Tightening (QT) coincides with the rebuilding of the Treasury cash account. Please find IVI’s full analysis below:

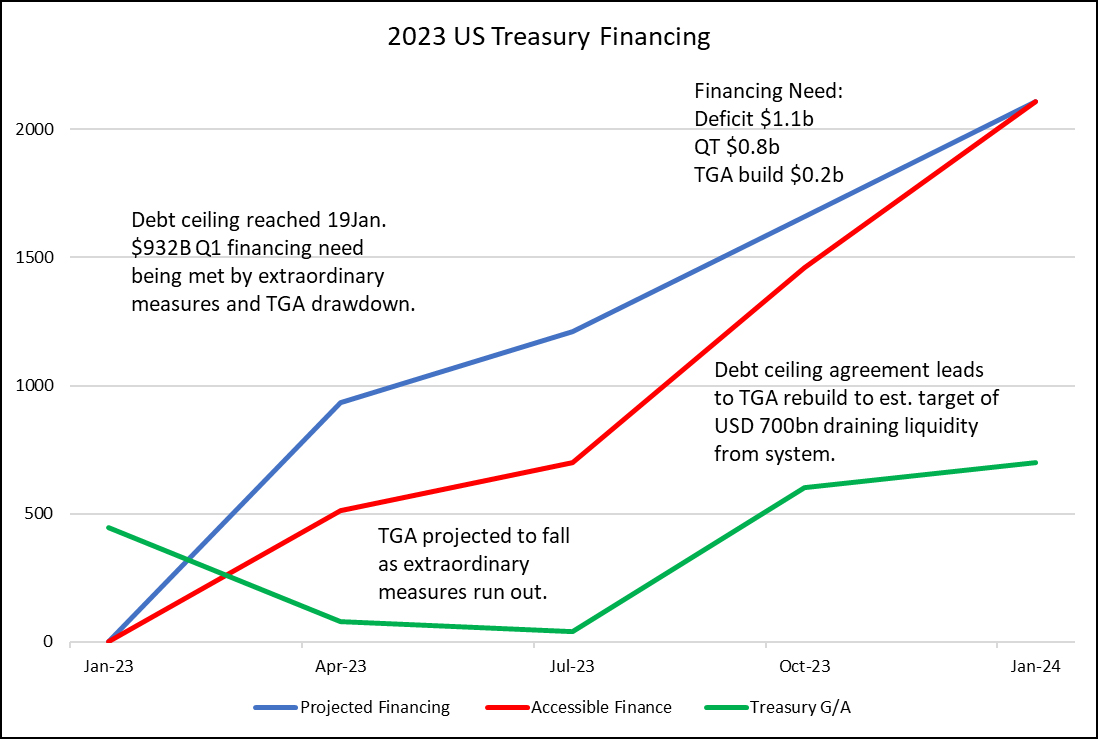

On January 19, 2023, the US reached its statutory debt limit which needs to be raised by Congress. We see the politically charged debt ceiling impasse as likely to go down to the last minute before resolution. So how does the US pay its obligations in the interim? Initially, they will keep issuing debt as scheduled, utilizing ‘extraordinary measures’. This allows them to turn certain outstanding debt into IOUs and thereby lowering the amount of debt subject to the limit. Smoke and mirrors accountancy. Once extraordinary measures are exhausted, they will turn to paying cash out from the Treasury’s General Account (TGA) held at the Fed which currently stands at USD 490bio.

Once that is second route is exhausted, three options remain. Either the US defaults, is forced to prioritize payments between debt repayments or entitlements such as salaries, social security, pensions etc, or Congress breaks the impasse and raises the debt ceiling. We see June 2023 as the ‘drop dead’ date for this process.

From a liquidity perspective, what matters is the TGA dynamic. The longer the impasse continues, the more the TGA will have to be drawn down. Whilst funds are being withdrawn from the TGA it has a counter effect to Quantitative Tightening (QT); payments of cash are made with no new debt being issued. Critically, (if!) when the impasse is resolved we estimate the TGA will need to be replenished to USD 550-700bio.

This will rapidly remove cash from the system. When combined with QT, it will greatly tighten US liquidity conditions at the same time Europe is embarking on QT and the Bank of Japan may further pullback on yield curve control. Even if the US economy is slowing by this summer point, the nature of the debt dynamics means a liquidity-driven ‘rescue’ plan for financial markets is at odds with the inflation targets of central banks. This is creating conditions ripe for risk decompression, a rapid tightening of conditions driving risk assets lower, and a significant pick up in volatility of markets through 2023.

IVI Capital on C8 Studio

.